The Future of Scalable Design in Banking

Why growth without architectural discipline is not growth it is debt with a product roadmap

Chemss Salem

Every major bank I've worked with or alongside in the past decade has a version of the same problem. They can serve their existing customer base competently. They have invested in digital channels, launched mobile applications, modernised parts of their compliance stack. But when genuine scale is required a new market, a regulatory shift, an acquisition, a tenfold increase in transaction volume the cracks appears.

The interfaces hold. The branding is consistent. And then something breaks in the engine room: a data pipeline that was never built for real-time load, an approval workflow hardcoded into a legacy system nobody fully understands, a design pattern that was created for one product and now needs to work across twelve.

The problem is not a lack of investment. Most of these institutions have spent considerably on digital transformation. The problem is that they have been optimising for the present scale while building toward a future that requires a different kind of foundation entirely.

Scalable design in banking is not a technical concept dressed up in UX language. It is a strategic posture a set of architectural, operational, and governance decisions that determine whether growth is sustainable or whether it systematically produces new forms of fragility.

CORE ARGUMENT

A bank that performs well at 100,000 users and breaks at 10 million did not have a scaling problem. It had a design problem that was invisible at low volume. The conditions for failure were built in from the start.

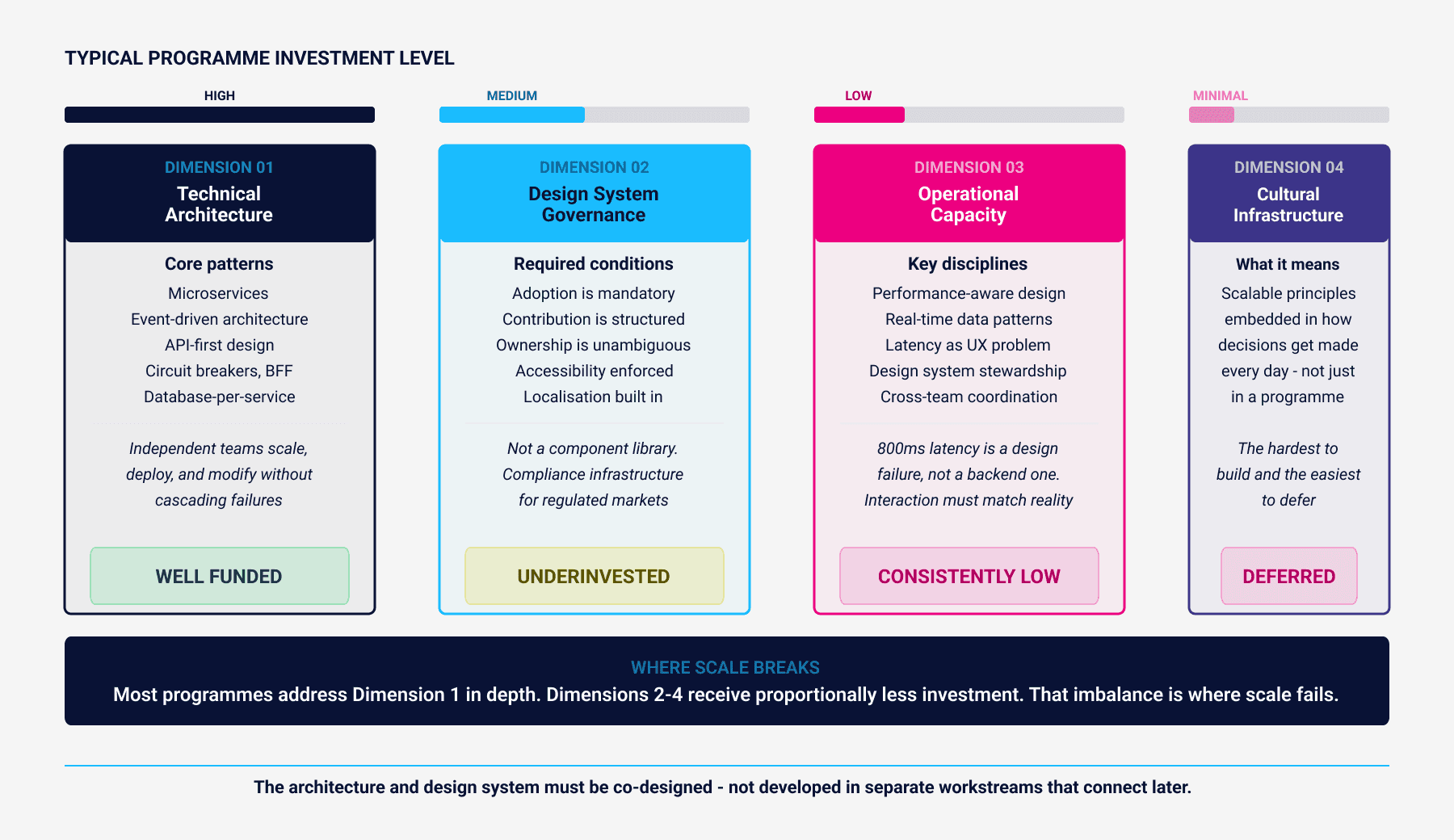

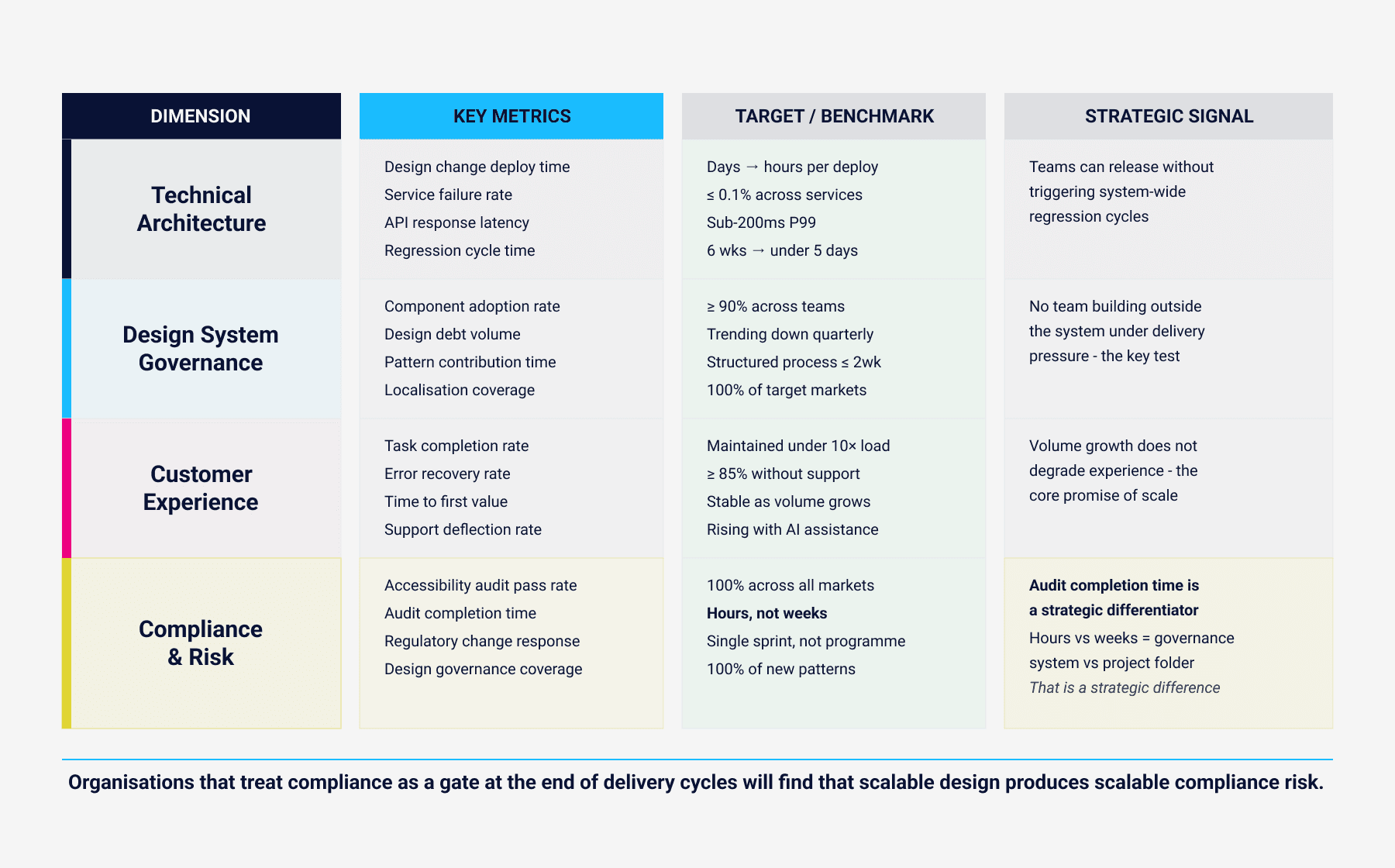

1. What Scalable Design Actually Means

The term gets misused. In most executive conversations, scalable means bigger more users, more transactions, more markets. That is volume scaling, and it is the easy part to conceptualise.

Real scalability has two distinct dimensions that most transformation programmes conflate or ignore entirely.

From an operational standpoint: the system supports growing user volumes, expanding transaction loads, and new regulatory requirements without losing efficiency or reliability. This is fundamentally an architecture and infrastructure question.

From a design standpoint: new products, journeys, and interfaces can be launched rapidly while maintaining coherence, accessibility, and quality. This is a governance and systems question not a visual one.

The second dimension is where most banks underinvest. They treat design as downstream of engineering, which means design debt accumulates quietly and surfaces only when the organisation tries to move fast on something new.

Scalable design, properly understood, is about building the conditions for consistent quality at velocity. That requires four interconnected dimensions to function together.

Most transformation programmes address dimension one technical architecture in significant depth. Dimensions two through four receive proportionally less investment and governance attention. That imbalance is where scale breaks down.

2. The Architecture Argument: Why Modularity Is Non-Negotiable

Monolithic core banking systems were built for a different era. They were designed to be stable, not adaptable. For decades, that was the correct trade-off. Stability in financial infrastructure is not a conservative preference it is a regulatory and operational necessity.

But stability and adaptability are no longer opposites. The financial services sector has demonstrated, through the growth of neobanks and platform-native competitors, that modular, API-first architecture can be both more resilient and more flexible than the monolithic systems it is designed to replace.

The microservices patterns that enterprise banking is now adopting Event-Driven Architecture, Circuit Breakers, Backend-for-Frontend (BFF), Saga Pattern, Database-per-Service are not engineering fashions. They are structural responses to a specific problem: how do you allow independent teams to scale, deploy, and modify discrete capabilities without triggering cascading failures across the whole system?

For design, the implication is direct. A modular backend architecture creates the conditions for a modular design system to actually work. You cannot maintain design consistency across independently deployed services if those services were never designed to share a common component layer. The architecture and the design system must be co-designed, not developed in separate workstreams that connect later.

FIELD OBSERVATION - EUROPEAN BANKING TRANSFORMATION

A European investment bank rebuilt its quantitative platform using microservices, decomposing a monolithic risk calculation engine into independently deployable services. The design implication was immediate: onboarding flows, data visualisation patterns, and error handling could be updated per-service without triggering system-wide regression cycles. Time to deploy a design change dropped from six weeks to four days.

3. Design Systems Are Infrastructure, Not Output

The banking sector has invested heavily in design systems over the past five years. Most of these investments have delivered inconsistent returns not because the systems were poorly designed, but because they were governed poorly.

A design system that is optional to adopt is not a design system. It is a component library with aspirational documentation. The distinction matters because optional systems do not scale. Teams under delivery pressure make local decisions. Exceptions multiply. The system fragments precisely when consistency is needed most during a platform expansion or a regulatory compliance sprint.

For design systems to function at banking scale, three governance conditions must hold:

Adoption is not optional. New product teams inherit the system; they do not start from scratch.

Contribution is structured. There is a defined process for proposing, reviewing, and integrating new patterns not a political negotiation between product teams.

Ownership is unambiguous. Someone is accountable for system health, deprecation cycles, and compliance with accessibility and localisation standards.

Without these conditions, a design system becomes an artefact that documents what the organisation wished it was doing, rather than a system that governs what it actually does.

In financial services, where regulatory environments vary by market and accessibility requirements are increasingly enforced, design system governance is compliance infrastructure. Treating it as a design team deliverable misses that point entirely.

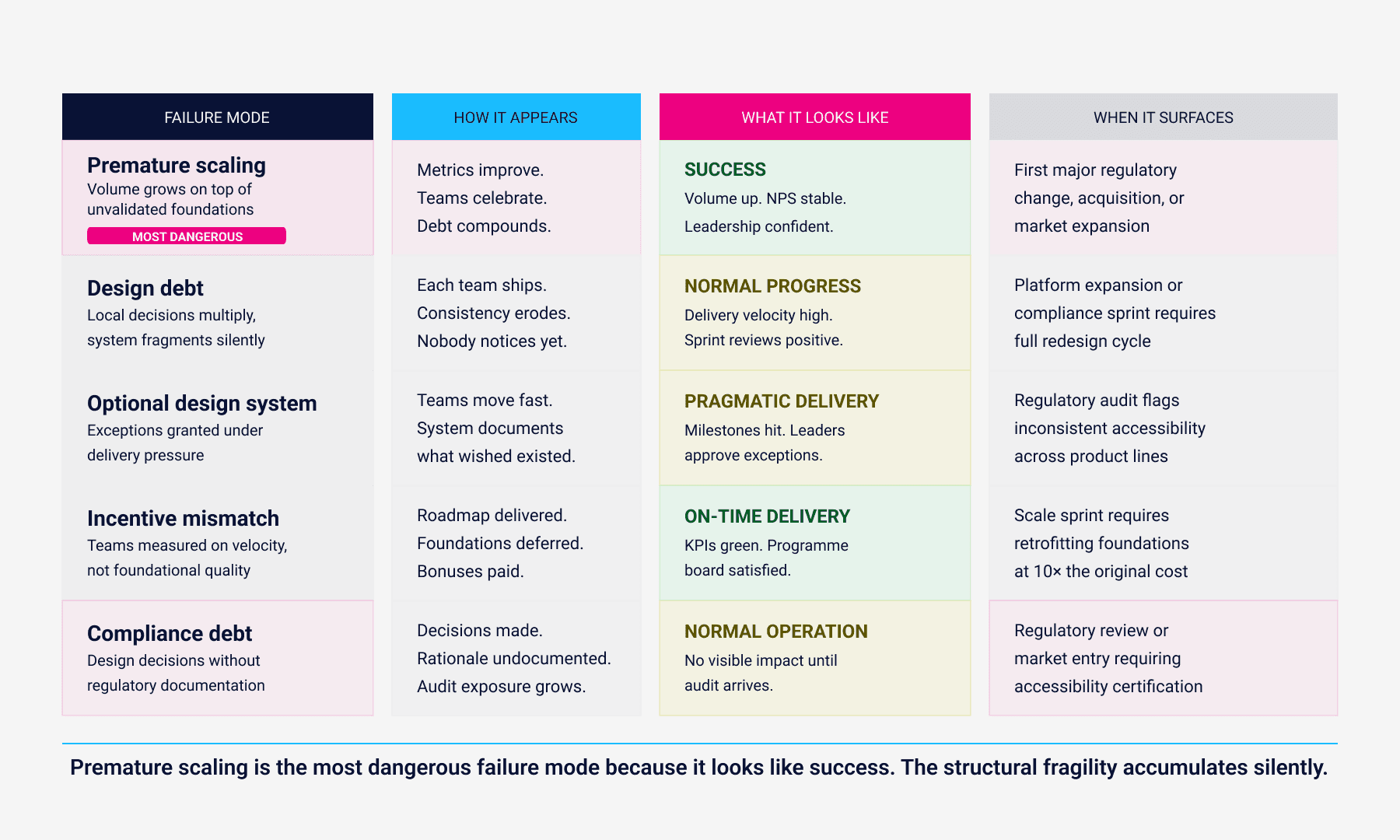

4. Where Scaling Actually Fails: The Honest Diagnosis

There is a version of the scalable design narrative that is too clean. Adopt microservices, build a design system, invest in API governance, and growth becomes frictionless. The real picture is messier.

Scaling breaks in specific, predictable places. Most of them are not technical. They are organisational.

The pattern that I encounter most consistently across banking and energy platform programmes is the gap between what the architecture roadmap says and what the organisational incentive structure rewards. Teams are measured on delivery velocity. Scalable design which requires investment in foundations before it pays off in speed looks like overhead until it is obviously too late to retrofit.

Premature scaling is the most dangerous failure mode because it looks like success. Volume grows. Metrics improve. And the structural fragility accumulates silently until the first major regulatory change, acquisition, or market expansion exposes it.

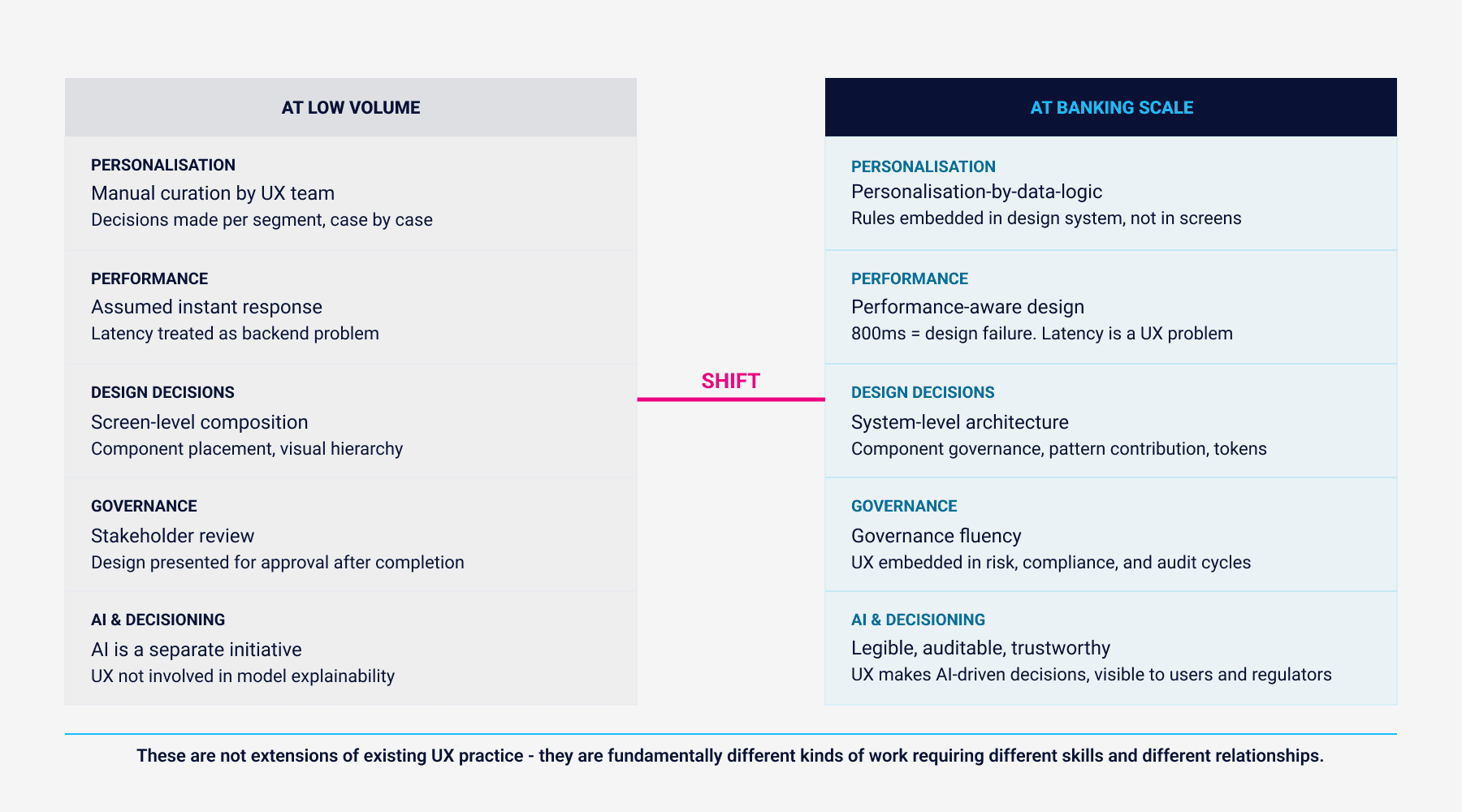

5. The UX Professional's Specific Responsibility

For UX teams operating inside banking institutions, scalable design introduces a set of responsibilities that go well beyond interaction design. These are not extensions of existing practice they are fundamentally different kinds of work that require different skills, different relationships with engineering and product, and a different posture toward governance.

The shift from personalisation-by-manual-curation to personalisation-by-data-logic deserves particular attention in the banking context. At low volume, UX teams can make individual decisions about which content surfaces to which user segment. At millions of users across multiple markets, this is architecturally impossible without embedding personalisation logic directly into the design system as rules, not as screens.

Performance-aware design is the other discipline that banking UX teams consistently underweight. In energy and financial services platforms where real-time data processing is central to the user experience trading interfaces, fraud alert flows, credit decisioning latency is a design problem, not a backend problem. If the interaction pattern assumes instant response and the system delivers 800ms, the design has failed regardless of how well the component looks.

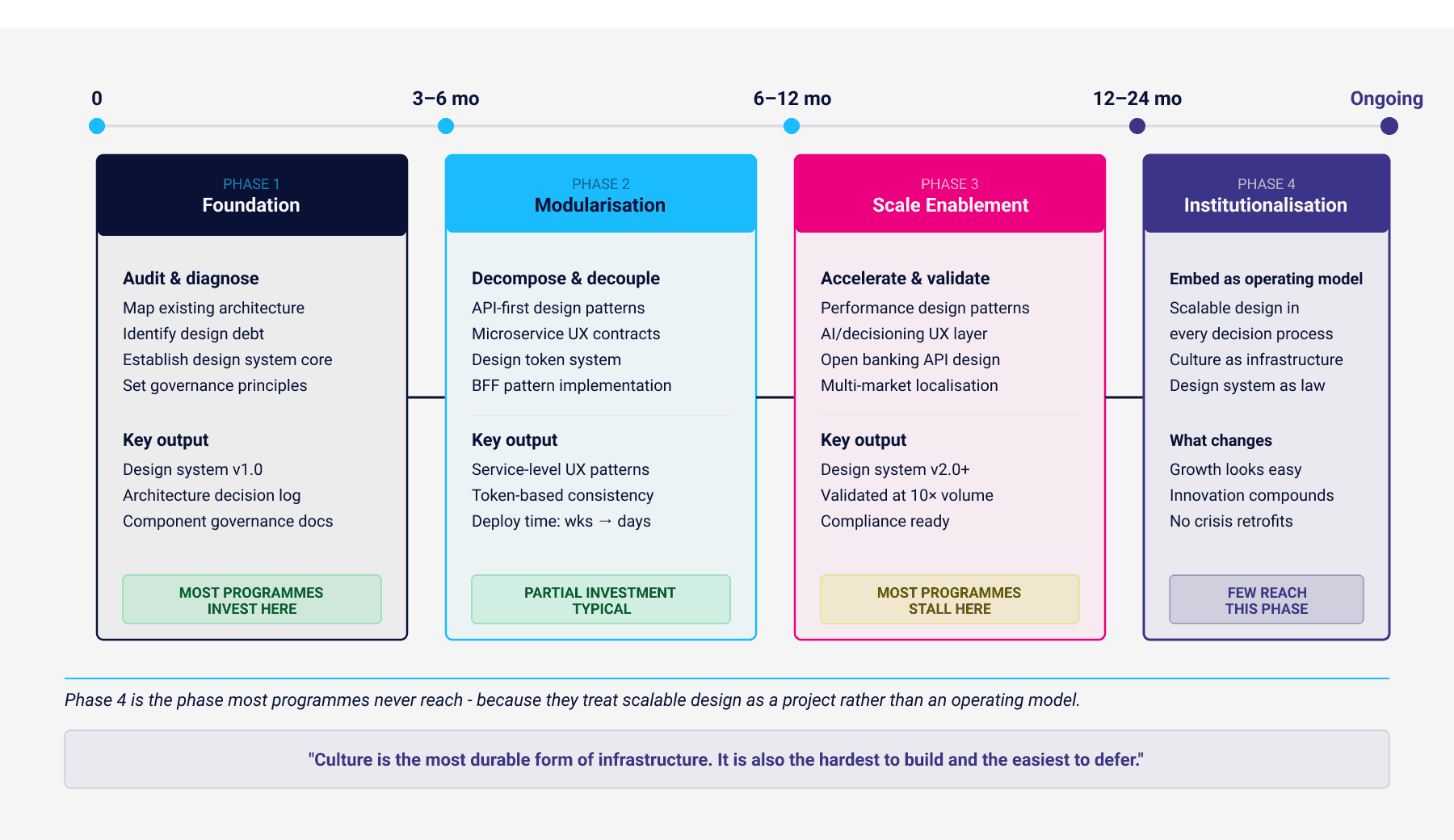

6. Building for Scale: A Practical Roadmap

Scalable design is not achieved in a single programme cycle. It is built through phased, disciplined investment that prioritises foundation over velocity in the early stages which is exactly why most organisations resist it.

Phase 4 - institutionalisation is the phase most programmes never reach, because they treat scalable design as a project rather than an operating model. The organisations that consistently produce good user experiences at scale are not the ones that ran the best transformation programme. They are the ones that embedded scalable design principles into how decisions get made every day.

Culture is the most durable form of infrastructure. It is also the hardest to build and the easiest to defer.

7. Measuring What Actually Matters

Scalable design cannot be governed without metrics that reflect the full picture. Most banking institutions measure system performance and customer experience in isolation. The organisations that scale effectively connect these layers into a unified view.

The compliance and risk row deserves specific attention in the banking context. Risk governance is not a separate track from scalable design it is embedded in it. Every architectural decision, every design pattern, every automation layer carries regulatory implications. Organisations that treat compliance as a gate at the end of delivery cycles will find that scalable design produces scalable compliance risk.

Audit completion time is a particularly revealing metric. A bank whose design system has proper accessibility and localisation documentation can respond to a regulatory audit in hours. A bank whose design decisions are distributed across product teams with no shared governance can take weeks. That is not an operational difference. It is a strategic one.

8. The Forces That Will Reshape the Next Decade

The pressures driving banking institutions toward scalable design are not easing. Several structural forces will intensify over the next ten years, and they will reward organisations that built the right foundations and expose those that did not.

Cloud-native infrastructure and elastic scalability

Hybrid and multi-cloud models are becoming the default for tier-one banking. The design implication is significant: interface and service architecture must be cloud-agnostic by design, not retrofitted after platform decisions are made.

AI and real-time decisioning embedded in UX

Enterprise-wide AI deployment in credit scoring, fraud detection, and customer support is already underway in the institutions I follow closely. The UX challenge is not the AI it is designing interfaces that make AI-driven decisions legible, auditable, and trustworthy to both users and regulators. That requires a different kind of design thinking than screen composition.

Open banking and embedded finance

API ecosystems are becoming competitive infrastructure. Banks that publish well-governed developer APIs can scale through partnerships rather than internal buildout. Design systems that expose their logic through APIs not just their visual components are the ones that will power this layer.

Sustainable finance integration

ESG reporting requirements are moving from voluntary to mandatory across major markets. Banking platforms that have scalable data architectures will be able to integrate ESG metrics without full programme cycles. Those built on fragmented legacy systems will treat it as another crisis migration.

Hyper-personalisation at population scale

The promise of AI-driven personalisation serving millions of users an experience calibrated to their specific context, behaviour, and needs is not a future state. It is a current competitive differentiator for the most advanced institutions. Getting there requires the data platforms, governance frameworks, and design system logic that most banks are still building.

9. The Honest Assessment

Scalable design is not a feature of well-run programmes. It is a precondition for sustainable growth in an industry where the cost of getting it wrong in regulatory exposure, operational fragility, and user trust is measured in years and hundreds of millions.

The banks that will define the next era of financial services are not the ones with the most innovative front-end experiences. They are the ones that built the architectural, governance, and design foundations that allow innovation to compound rather than accumulate debt.

The choice is not between speed and scalability. It is between investing in scalability now, as a deliberate programme decision, or paying for it later as a crisis response.

The organisations that master this distinction will not just grow. They will make growth look easy because they built the conditions for it before they needed them.

CLOSING STATEMENT

In modern banking, scale is not the outcome. It is the strategy. And strategy without architecture is just aspiration with a delivery date.

References

UXDA (2025). How Product Design Increases Bank Profits.

McKinsey & Company (2021). Building the AI Bank of the Future.

IJERET (2024). Scalable Microservices Design Patterns in Banking Architecture.

Adria-BT (2025). Building a Future-Proof Digital Banking Infrastructure.

ArXiv (2024). Open Banking and Digital Ecosystems.

About the Author

Chemsseddine SALEM is a Lead UX Designer and Researcher specialising in Enterprise SaaS, UX Governance, Finance, and Energy sectors. He is the founder of Chemss Labs and works with organisations navigating large-scale digital transfo

About

Featured Posts

Related Post

Why simplicity is a luxury, systems thinking is survival, and the UX leader's real job is sense-making at scale

Role drift, assumption-driven design, and the organisational cost of confusing familiarity with expertise

Discover the 2026 UX trends transforming design AI-driven interfaces, inclusive experiences, and sustainable innovation.

Designing trust in UX means crafting clarity, transparency, and accountability, especially in finance, energy, and healthcare industries.